Conditional Average Treatment Effects (CATE) with DoWhy and EconML

This is an experimental feature where we use EconML methods from DoWhy. Using EconML allows CATE estimation using different methods.

All four steps of causal inference in DoWhy remain the same: model, identify, estimate, and refute. The key difference is that we now call econml methods in the estimation step. There is also a simpler example using linear regression to understand the intuition behind CATE estimators.

All datasets are generated using linear structural equations.

[1]:

import numpy as np

import pandas as pd

import logging

import dowhy

from dowhy import CausalModel

import dowhy.datasets

import econml

import warnings

warnings.filterwarnings('ignore')

BETA = 10

[2]:

data = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=2, num_effect_modifiers=2,

num_treatments=1,

treatment_is_binary=False,

num_discrete_common_causes=2,

num_discrete_effect_modifiers=0,

one_hot_encode=False)

df=data['df']

print(df.head())

print("True causal estimate is", data["ate"])

X0 X1 Z0 Z1 W0 W1 W2 W3 v0 \

0 1.898922 -1.493600 1.0 0.093164 0.097720 0.440277 3 2 22.528813

1 0.885180 -2.027130 0.0 0.790633 0.203576 -0.210274 2 2 16.619325

2 0.379053 -0.216526 0.0 0.049098 -0.453768 -0.439534 0 3 -1.908925

3 1.384133 1.860552 0.0 0.224985 1.216297 0.075126 1 0 7.027797

4 0.803883 -1.275331 1.0 0.511890 0.302380 1.060172 2 0 24.172841

y

0 357.902396

1 199.083575

2 -21.889854

3 117.426939

4 296.879249

True causal estimate is 11.13817451301838

[3]:

model = CausalModel(data=data["df"],

treatment=data["treatment_name"], outcome=data["outcome_name"],

graph=data["gml_graph"])

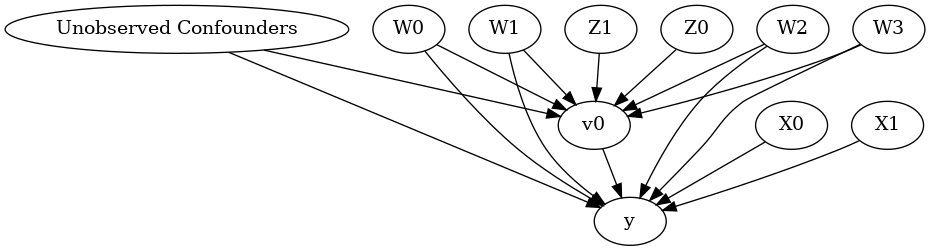

[4]:

model.view_model()

from IPython.display import Image, display

display(Image(filename="causal_model.png"))

[5]:

identified_estimand= model.identify_effect(proceed_when_unidentifiable=True)

print(identified_estimand)

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

### Estimand : 2

Estimand name: iv

Estimand expression:

Expectation(Derivative(y, [Z1, Z0])*Derivative([v0], [Z1, Z0])**(-1))

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z1,Z0})

Estimand assumption 2, Exclusion: If we remove {Z1,Z0}→{v0}, then ¬({Z1,Z0}→y)

### Estimand : 3

Estimand name: frontdoor

No such variable found!

Linear Model

First, let us build some intuition using a linear model for estimating CATE. The effect modifiers (that lead to a heterogeneous treatment effect) can be modeled as interaction terms with the treatment. Thus, their value modulates the effect of treatment.

Below the estimated effect of changing treatment from 0 to 1.

[6]:

linear_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.linear_regression",

control_value=0,

treatment_value=1)

print(linear_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0+v0*X1+v0*X0

Target units: ate

## Estimate

Mean value: 11.138323583866043

### Conditional Estimates

__categorical__X1 __categorical__X0

(-3.742, -1.16] (-3.816, -0.439] 5.350980

(-0.439, 0.172] 8.452173

(0.172, 0.677] 10.231967

(0.677, 1.246] 11.996779

(1.246, 4.411] 14.906734

(-1.16, -0.589] (-3.816, -0.439] 5.981074

(-0.439, 0.172] 8.985925

(0.172, 0.677] 10.909247

(0.677, 1.246] 12.577942

(1.246, 4.411] 15.509218

(-0.589, -0.1] (-3.816, -0.439] 6.582177

(-0.439, 0.172] 9.335388

(0.172, 0.677] 11.190280

(0.677, 1.246] 12.909711

(1.246, 4.411] 15.754069

(-0.1, 0.472] (-3.816, -0.439] 6.810293

(-0.439, 0.172] 9.691918

(0.172, 0.677] 11.559779

(0.677, 1.246] 13.262256

(1.246, 4.411] 16.144426

(0.472, 3.296] (-3.816, -0.439] 7.313792

(-0.439, 0.172] 10.285809

(0.172, 0.677] 12.091017

(0.677, 1.246] 13.846789

(1.246, 4.411] 16.792039

dtype: float64

EconML methods

We now move to the more advanced methods from the EconML package for estimating CATE.

First, let us look at the double machine learning estimator. Method_name corresponds to the fully qualified name of the class that we want to use. For double ML, it is “econml.dml.DML”.

Target units defines the units over which the causal estimate is to be computed. This can be a lambda function filter on the original dataframe, a new Pandas dataframe, or a string corresponding to the three main kinds of target units (“ate”, “att” and “atc”). Below we show an example of a lambda function.

Method_params are passed directly to EconML. For details on allowed parameters, refer to the EconML documentation.

[7]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = lambda df: df["X0"]>1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=False)},

"fit_params":{}})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0 | X1,X0

Target units: Data subset defined by a function

## Estimate

Mean value: 15.15260356848542

Effect estimates: [15.33955778 15.84879232 14.66910411 ... 18.4715256 14.39605376

17.57646996]

[8]:

print("True causal estimate is", data["ate"])

True causal estimate is 11.13817451301838

[9]:

dml_estimate = model.estimate_effect(identified_estimand, method_name="backdoor.econml.dml.DML",

control_value = 0,

treatment_value = 1,

target_units = 1, # condition used for CATE

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0 | X1,X0

Target units:

## Estimate

Mean value: 11.037725784237395

Effect estimates: [15.27390981 11.5084465 11.0123769 ... 7.07033426 11.24713532

10.45835842]

CATE Object and Confidence Intervals

EconML provides its own methods to compute confidence intervals. Using BootstrapInference in the example below.

[10]:

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LassoCV

from sklearn.ensemble import GradientBoostingRegressor

from econml.inference import BootstrapInference

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = "ate",

confidence_intervals=True,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final": LassoCV(fit_intercept=False),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{

'inference': BootstrapInference(n_bootstrap_samples=100, n_jobs=-1),

}

})

print(dml_estimate)

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0 | X1,X0

Target units: ate

## Estimate

Mean value: 11.03107854161636

Effect estimates: [15.23154757 11.4914362 11.00644985 ... 7.09605105 11.23996513

10.45151404]

95.0% confidence interval: (array([15.20814535, 11.43427515, 10.97728669, ..., 6.92179496,

11.21199051, 10.40377708]), array([15.53654796, 11.69017454, 11.10728956, ..., 7.17041884,

11.35021865, 10.56899233]))

Can provide a new inputs as target units and estimate CATE on them.

[11]:

test_cols= data['effect_modifier_names'] # only need effect modifiers' values

test_arr = [np.random.uniform(0,1, 10) for _ in range(len(test_cols))] # all variables are sampled uniformly, sample of 10

test_df = pd.DataFrame(np.array(test_arr).transpose(), columns=test_cols)

dml_estimate = model.estimate_effect(identified_estimand,

method_name="backdoor.econml.dml.DML",

target_units = test_df,

confidence_intervals=False,

method_params={"init_params":{'model_y':GradientBoostingRegressor(),

'model_t': GradientBoostingRegressor(),

"model_final":LassoCV(),

'featurizer':PolynomialFeatures(degree=1, include_bias=True)},

"fit_params":{}

})

print(dml_estimate.cate_estimates)

[11.09338659 12.13565105 11.3207331 12.64976079 13.0817584 12.11993925

11.57045914 11.44465176 13.48497597 11.05031631]

Can also retrieve the raw EconML estimator object for any further operations

[12]:

print(dml_estimate._estimator_object)

<econml.dml.dml.DML object at 0x7f516ff479d0>

Works with any EconML method

In addition to double machine learning, below we example analyses using orthogonal forests, DRLearner (bug to fix), and neural network-based instrumental variables.

Binary treatment, Binary outcome

[13]:

data_binary = dowhy.datasets.linear_dataset(BETA, num_common_causes=4, num_samples=10000,

num_instruments=2, num_effect_modifiers=2,

treatment_is_binary=True, outcome_is_binary=True)

# convert boolean values to {0,1} numeric

data_binary['df'].v0 = data_binary['df'].v0.astype(int)

data_binary['df'].y = data_binary['df'].y.astype(int)

print(data_binary['df'])

model_binary = CausalModel(data=data_binary["df"],

treatment=data_binary["treatment_name"], outcome=data_binary["outcome_name"],

graph=data_binary["gml_graph"])

identified_estimand_binary = model_binary.identify_effect(proceed_when_unidentifiable=True)

X0 X1 Z0 Z1 W0 W1 W2 \

0 0.607055 -1.614792 1.0 0.455616 1.221222 -0.648731 1.326302

1 2.993224 -0.200924 0.0 0.311552 -0.804113 0.837046 -0.219313

2 1.991809 1.339323 0.0 0.177437 0.541844 -1.252206 -0.018509

3 1.375978 0.476735 1.0 0.549200 -1.052208 -1.242290 0.363920

4 0.802443 -0.904535 0.0 0.348527 1.370334 -0.536766 -0.011914

... ... ... ... ... ... ... ...

9995 -0.376158 -0.719342 0.0 0.213180 -0.463657 -1.072515 -1.974591

9996 0.116404 2.395842 0.0 0.153815 1.254356 -1.060713 1.624262

9997 0.514493 -0.307350 1.0 0.048421 -0.141551 0.897432 -0.602098

9998 0.715935 -1.660456 0.0 0.895173 -0.653106 2.064832 -0.931449

9999 1.145919 -1.137355 1.0 0.068377 1.188003 -0.917376 -0.878206

W3 v0 y

0 -0.496089 1 1

1 -0.455882 0 1

2 0.276731 1 1

3 0.027972 1 1

4 -0.133733 1 1

... ... .. ..

9995 -1.383749 0 0

9996 -0.553284 1 1

9997 -0.602913 1 1

9998 0.302548 1 1

9999 -0.008667 1 1

[10000 rows x 10 columns]

Using DRLearner estimator

[14]:

from sklearn.linear_model import LogisticRegressionCV

#todo needs binary y

drlearner_estimate = model_binary.estimate_effect(identified_estimand_binary,

method_name="backdoor.econml.drlearner.LinearDRLearner",

confidence_intervals=False,

method_params={"init_params":{

'model_propensity': LogisticRegressionCV(cv=3, solver='lbfgs', multi_class='auto')

},

"fit_params":{}

})

print(drlearner_estimate)

print("True causal estimate is", data_binary["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,W1,X1,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,W1,X1,X0,W0,U) = P(y|v0,W3,W2,W1,X1,X0,W0)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0 | X1,X0

Target units: ate

## Estimate

Mean value: 0.48099941411381597

Effect estimates: [0.34133643 0.58394521 0.69402234 ... 0.46721726 0.34146445 0.41183014]

True causal estimate is 0.3833

Instrumental Variable Method

[15]:

import keras

from econml.deepiv import DeepIVEstimator

dims_zx = len(model._instruments)+len(model._effect_modifiers)

dims_tx = len(model._treatment)+len(model._effect_modifiers)

treatment_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(dims_zx,)), # sum of dims of Z and X

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17)])

response_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(dims_tx,)), # sum of dims of T and X

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(1)])

deepiv_estimate = model.estimate_effect(identified_estimand,

method_name="iv.econml.deepiv.DeepIV",

target_units = lambda df: df["X0"]>-1,

confidence_intervals=False,

method_params={"init_params":{'n_components': 10, # Number of gaussians in the mixture density networks

'm': lambda z, x: treatment_model(keras.layers.concatenate([z, x])), # Treatment model,

"h": lambda t, x: response_model(keras.layers.concatenate([t, x])), # Response model

'n_samples': 1, # Number of samples used to estimate the response

'first_stage_options': {'epochs':25},

'second_stage_options': {'epochs':25}

},

"fit_params":{}})

print(deepiv_estimate)

Using TensorFlow backend.

Epoch 1/25

10000/10000 [==============================] - 2s 158us/step - loss: 6.0581

Epoch 2/25

10000/10000 [==============================] - 1s 90us/step - loss: 2.5423

Epoch 3/25

10000/10000 [==============================] - 1s 88us/step - loss: 2.3626

Epoch 4/25

10000/10000 [==============================] - 1s 87us/step - loss: 2.3099

Epoch 5/25

10000/10000 [==============================] - 1s 87us/step - loss: 2.2638

Epoch 6/25

10000/10000 [==============================] - 1s 99us/step - loss: 2.2351

Epoch 7/25

10000/10000 [==============================] - 1s 94us/step - loss: 2.2353

Epoch 8/25

10000/10000 [==============================] - 1s 83us/step - loss: 2.2118

Epoch 9/25

10000/10000 [==============================] - 1s 84us/step - loss: 2.2095

Epoch 10/25

10000/10000 [==============================] - 1s 83us/step - loss: 2.1964

Epoch 11/25

10000/10000 [==============================] - 1s 83us/step - loss: 2.1899

Epoch 12/25

10000/10000 [==============================] - 1s 99us/step - loss: 2.1810

Epoch 13/25

10000/10000 [==============================] - 1s 110us/step - loss: 2.1768

Epoch 14/25

10000/10000 [==============================] - 1s 107us/step - loss: 2.1662

Epoch 15/25

10000/10000 [==============================] - 1s 97us/step - loss: 2.1600

Epoch 16/25

10000/10000 [==============================] - 1s 81us/step - loss: 2.1619

Epoch 17/25

10000/10000 [==============================] - 1s 89us/step - loss: 2.1534

Epoch 18/25

10000/10000 [==============================] - 1s 105us/step - loss: 2.1529

Epoch 19/25

10000/10000 [==============================] - 1s 96us/step - loss: 2.1530

Epoch 20/25

10000/10000 [==============================] - 1s 104us/step - loss: 2.1509

Epoch 21/25

10000/10000 [==============================] - 1s 91us/step - loss: 2.1388

Epoch 22/25

10000/10000 [==============================] - 1s 88us/step - loss: 2.1440

Epoch 23/25

10000/10000 [==============================] - 1s 87us/step - loss: 2.1422

Epoch 24/25

10000/10000 [==============================] - 1s 94us/step - loss: 2.1302

Epoch 25/25

10000/10000 [==============================] - 1s 92us/step - loss: 2.1334

Epoch 1/25

10000/10000 [==============================] - 2s 197us/step - loss: 9634.7153

Epoch 2/25

10000/10000 [==============================] - 1s 124us/step - loss: 6117.5493

Epoch 3/25

10000/10000 [==============================] - 1s 132us/step - loss: 6080.0172

Epoch 4/25

10000/10000 [==============================] - 1s 144us/step - loss: 6000.0626

Epoch 5/25

10000/10000 [==============================] - 1s 140us/step - loss: 5903.0761

Epoch 6/25

10000/10000 [==============================] - 1s 114us/step - loss: 5971.7064

Epoch 7/25

10000/10000 [==============================] - 1s 109us/step - loss: 5927.9321

Epoch 8/25

10000/10000 [==============================] - 1s 107us/step - loss: 6042.7108

Epoch 9/25

10000/10000 [==============================] - 1s 107us/step - loss: 5935.9766

Epoch 10/25

10000/10000 [==============================] - 1s 108us/step - loss: 5899.0229

Epoch 11/25

10000/10000 [==============================] - 1s 108us/step - loss: 5814.6864

Epoch 12/25

10000/10000 [==============================] - 1s 110us/step - loss: 5938.3598

Epoch 13/25

10000/10000 [==============================] - 1s 110us/step - loss: 5783.8304

Epoch 14/25

10000/10000 [==============================] - 1s 110us/step - loss: 5861.9487

Epoch 15/25

10000/10000 [==============================] - 1s 122us/step - loss: 5884.3656

Epoch 16/25

10000/10000 [==============================] - 1s 145us/step - loss: 5875.7650

Epoch 17/25

10000/10000 [==============================] - 1s 131us/step - loss: 5842.4607

Epoch 18/25

10000/10000 [==============================] - 1s 117us/step - loss: 5833.5643

Epoch 19/25

10000/10000 [==============================] - 1s 123us/step - loss: 5883.4645

Epoch 20/25

10000/10000 [==============================] - 1s 110us/step - loss: 5888.1516

Epoch 21/25

10000/10000 [==============================] - 1s 111us/step - loss: 5883.6870

Epoch 22/25

10000/10000 [==============================] - 1s 111us/step - loss: 5917.5608

Epoch 23/25

10000/10000 [==============================] - 1s 114us/step - loss: 5954.1094

Epoch 24/25

10000/10000 [==============================] - 1s 110us/step - loss: 5871.8566

Epoch 25/25

10000/10000 [==============================] - 1s 117us/step - loss: 5842.7111

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: iv

Estimand expression:

Expectation(Derivative(y, [Z1, Z0])*Derivative([v0], [Z1, Z0])**(-1))

Estimand assumption 1, As-if-random: If U→→y then ¬(U →→{Z1,Z0})

Estimand assumption 2, Exclusion: If we remove {Z1,Z0}→{v0}, then ¬({Z1,Z0}→y)

## Realized estimand

b: y~v0+W3+W2+W1+X1+X0+W0 | X1,X0

Target units: Data subset defined by a function

## Estimate

Mean value: 3.3913748264312744

Effect estimates: [4.111145 2.1927567 4.0210876 ... 0.9122124 4.053177 2.2825317]

Metalearners

[16]:

data_experiment = dowhy.datasets.linear_dataset(BETA, num_common_causes=5, num_samples=10000,

num_instruments=2, num_effect_modifiers=5,

treatment_is_binary=True, outcome_is_binary=False)

# convert boolean values to {0,1} numeric

data_experiment['df'].v0 = data_experiment['df'].v0.astype(int)

print(data_experiment['df'])

model_experiment = CausalModel(data=data_experiment["df"],

treatment=data_experiment["treatment_name"], outcome=data_experiment["outcome_name"],

graph=data_experiment["gml_graph"])

identified_estimand_experiment = model_experiment.identify_effect(proceed_when_unidentifiable=True)

X0 X1 X2 X3 X4 Z0 Z1 \

0 -1.511404 -0.796794 0.381156 0.546913 0.988627 1.0 0.945576

1 1.084781 -1.922791 -0.461289 -0.208160 -1.362516 0.0 0.631043

2 -0.993879 0.264821 2.495885 0.768880 -0.200069 1.0 0.564980

3 -2.752826 -1.278350 2.013659 0.225430 -0.296333 1.0 0.729429

4 -0.176540 -0.143080 -1.994730 1.445114 -1.310322 0.0 0.660578

... ... ... ... ... ... ... ...

9995 -0.615514 -0.054405 -1.403155 0.047062 0.668092 0.0 0.049970

9996 -0.079075 -1.970365 0.590612 0.129645 1.702936 0.0 0.006828

9997 -0.612788 -1.583195 -0.955393 0.139663 0.633461 0.0 0.622620

9998 -2.649140 -1.605903 -1.236836 -1.253810 -1.396432 0.0 0.394677

9999 -1.006696 0.406869 -0.687812 0.247259 0.680919 0.0 0.069656

W0 W1 W2 W3 W4 v0 y

0 0.083088 -0.950762 0.474662 1.346305 -1.790676 1 1.968666

1 -0.082310 -0.659660 1.051546 1.581745 0.195329 1 10.434861

2 1.221314 -0.894577 0.308504 -0.166613 -1.599631 1 13.105967

3 1.151428 -1.390558 2.628862 0.928396 -0.477143 1 5.665644

4 0.299112 -0.227596 1.117443 0.333261 0.822112 1 9.385864

... ... ... ... ... ... .. ...

9995 0.688683 -1.733233 1.168689 -0.755424 -0.560150 0 -1.992805

9996 -0.396265 1.375946 0.622630 1.124654 0.143208 1 14.094986

9997 0.726669 -0.896359 2.831088 1.560724 -1.672692 1 8.784501

9998 -0.738313 -1.374355 1.775307 0.559349 -1.305286 1 -10.959509

9999 1.175807 -0.233245 2.094218 -0.437447 -0.219961 1 13.028082

[10000 rows x 14 columns]

[17]:

from sklearn.ensemble import RandomForestRegressor

metalearner_estimate = model_experiment.estimate_effect(identified_estimand_experiment,

method_name="backdoor.econml.metalearners.TLearner",

confidence_intervals=False,

method_params={"init_params":{

'models': RandomForestRegressor()

},

"fit_params":{}

})

print(metalearner_estimate)

print("True causal estimate is", data_experiment["ate"])

*** Causal Estimate ***

## Identified estimand

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

d

─────(Expectation(y|W3,W2,X4,W1,X3,X1,X2,W4,X0,W0))

d[v₀]

Estimand assumption 1, Unconfoundedness: If U→{v0} and U→y then P(y|v0,W3,W2,X4,W1,X3,X1,X2,W4,X0,W0,U) = P(y|v0,W3,W2,X4,W1,X3,X1,X2,W4,X0,W0)

## Realized estimand

b: y~v0+X3+X2+X1+X4+X0+W3+W2+W1+W4+W0

Target units: ate

## Estimate

Mean value: 6.287323303624039

Effect estimates: [ 4.61465613 12.53217671 8.69905637 ... 6.04112821 -3.265252

6.54000794]

True causal estimate is 5.535602451644429

Refuting the estimate

Adding a random common cause variable

[18]:

res_random=model.refute_estimate(identified_estimand, dml_estimate, method_name="random_common_cause")

print(res_random)

Refute: Add a Random Common Cause

Estimated effect:11.995163235677346

New effect:12.028609904102334

Adding an unobserved common cause variable

[19]:

res_unobserved=model.refute_estimate(identified_estimand, dml_estimate, method_name="add_unobserved_common_cause",

confounders_effect_on_treatment="linear", confounders_effect_on_outcome="linear",

effect_strength_on_treatment=0.01, effect_strength_on_outcome=0.02)

print(res_unobserved)

Refute: Add an Unobserved Common Cause

Estimated effect:11.995163235677346

New effect:12.046656228321476

Replacing treatment with a random (placebo) variable

[20]:

res_placebo=model.refute_estimate(identified_estimand, dml_estimate,

method_name="placebo_treatment_refuter", placebo_type="permute",

num_simulations=10 # at least 100 is good, setting to 10 for speed

)

print(res_placebo)

Refute: Use a Placebo Treatment

Estimated effect:11.995163235677346

New effect:0.014174758181060527

p value:0.40645666707426864

Removing a random subset of the data

[21]:

res_subset=model.refute_estimate(identified_estimand, dml_estimate,

method_name="data_subset_refuter", subset_fraction=0.8,

num_simulations=10)

print(res_subset)

Refute: Use a subset of data

Estimated effect:11.995163235677346

New effect:11.998974744372351

p value:0.46530895233272207

More refutation methods to come, especially specific to the CATE estimators.